Executive Summary

The defining story of the quarter was the economy’s resilience in the face of a severe oil shock and persistent geopolitical disruption, supported by strong household balance sheets, policy flexibility, China’s commodity stockpile drawdowns, and continued investment in AI infrastructure and energy capacity. At the same time, inflation remained the key risk, prompting a more hawkish Fed posture and raising the possibility that rates may stay higher for longer. For the rest of the year, strong earnings momentum and broader market participation are encouraging. Elevated inflation, Fed uncertainty, and wider dispersion within markets argue for disciplined diversification and active portfolio management.

A Resilient Economy Weathers the War, but Still Struggles With High Inflation

Perhaps the most important thing about the past quarter was what did not happen, which is that with crude oil prices increasing to a peak of $118.35 per barrel at the very start of the quarter, gasoline prices rising from below $3 per gallon to above $4.50, and with the Strait of Hormuz remaining closed effectively up until the end of the quarter, the economy did not experience a recession, nor did the equity market decline. This defied expectations from just about all commodity experts who, prior to this, would quite reasonably have listed the closure of the Strait for more than four months as an almost certain catalyst for a global recession.

Exactly why such a disaster did not occur came down to a combination of inventories, the waiving of Russian oil sanctions, demand destruction (across Southeast Asia, Australia, South Korea, and India, though not much in Europe or North America), and, importantly, China reducing its oil imports by about 40%.

China’s ability to draw down energy and other commodity stockpiles that had previously not been known about, was a major surprise, which greatly helped to provide global economic stability. One of the lessons from this crisis (which continues with news each day) is that countries should take a note out of China’s playbook and be prepared. In a new multipolar world, where access to raw materials can easily be blocked or face major disruptions, countries should make sure they have strategic reserves available for such events.

Also helping to stabilize the economy is that the U.S. consumer is, on the whole, very resilient, with strong household balance sheets and a structurally tight labor market. The U.S. is also in the midst of one of the largest capex booms in history, with billions of dollars being poured into a combination of AI infrastructure expansion (e.g., data centers) and energy production to support its development.

At William Blair’s 46th Annual Growth Stock Conference in June, we listened to company after company telling us that AI innovation and infrastructure expansion were still in their very early innings, and that the growth path still extends for many more years to come. The investment here is also spilling out across the industrial manufacturing sector—not only with regards to the buildout itself, but also with regards to demand from companies trying to offset ongoing labor shortages with automation and productivity improvements; upgrade an aging capital stock; and take advantage of government incentives to invest, such as accelerated depreciation allowances and, more controversially, tariffs.

The downside of this expenditure, however, is that it is also helping to keep inflationary pressures elevated. In this model, inflationary spending necessarily comes first, with the disinflationary productivity gains expected to follow, and we are still in the enabling phase and not yet in the adoption phase.

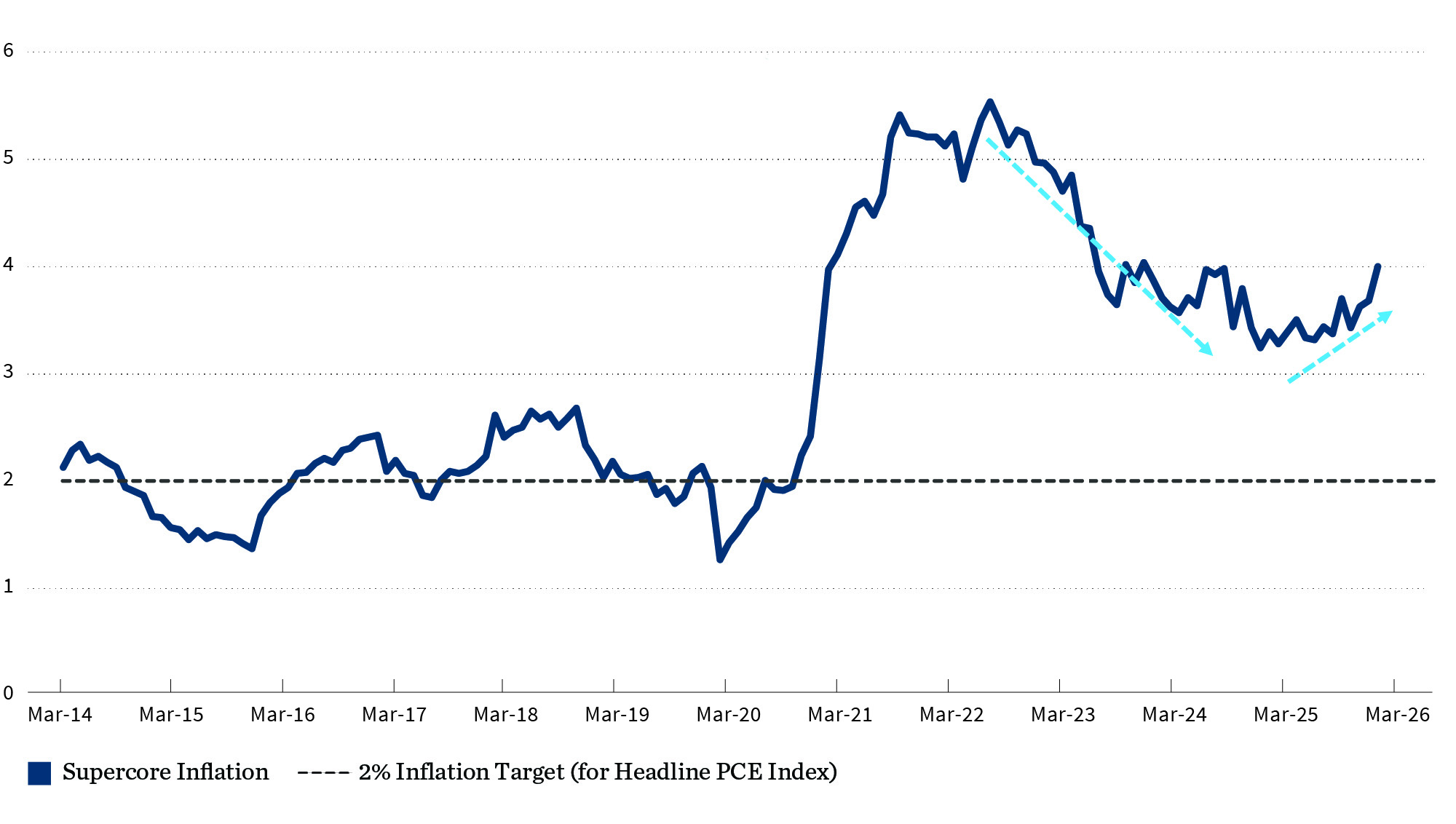

As we can see in exhibit 1, inflation has not only remained sticky, but it has actually accelerated. Unfortunately, what this exhibit also shows is that this reacceleration is not entirely the result of the conflict in the Middle East given that it started before its eruption. While the war has exacerbated the situation, it has only been one in a series of major supply-side shocks in the last five years that have continued to keep inflation elevated. These include: COVID, the war in Ukraine, tariffs, immigration restrictions, retiring baby boomers, reshoring/deglobalization, greater policy uncertainty, more tariffs, spending related to the OBBB, and the increased frequency of more extreme weather events (droughts, floods, fire, and hurricanes, with the unfolding super El Niño being just the latest example of this).

Supercore PCE Inflation – Services Less Energy & Housing

(% change on year ago)

More Hawkish Kevin Warsh Takes the Helm at the Fed

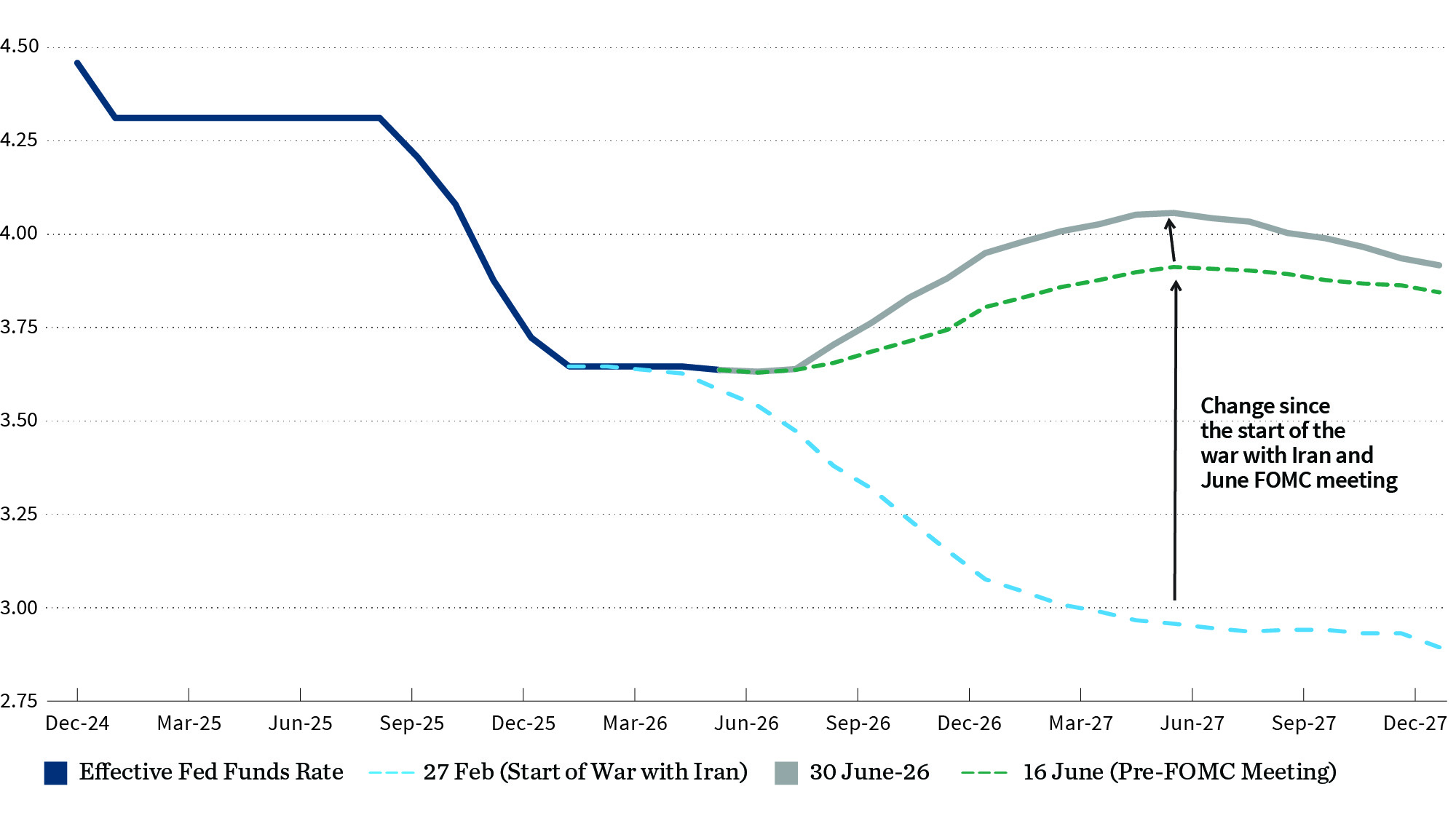

This inflation has not gone unnoticed by the newly minted Fed Chair Kevin Warsh, who stated in his first press conference (June 17) that we are now well into a sixth consecutive year of above-target inflation, and that his Fed plans to do something about it. The Committee’s much-shortened press statement ended with the strong final sentence: The Committee will deliver price stability. Yet, with the end of forward guidance, Chair Warsh is refusing to tell us what that something is (e.g. raising rates, shrinking the Fed’s balance sheet, or waiting for the expected disinflationary supply-side improvements from AI to kick in to do the heavy lifting).

Chair Warsh made a number of important announcements at this meeting, one of which was the ending of forward guidance (a tool that had effectively already been eliminated by the recurring so-called one-off supply shocks); the other was the establishment of a series of special taskforces erected to decide how the Fed should be going about the business of achieving its triple mandate of price stability, maximum employment, and moderate long-term interest rates. In other words, the taskforces are an attempt to assess what’s changed with the economy and financial markets, how we are measuring what’s happening, and what Fed policies create the intended impact or change. Until there is further clarity, the Fed may be viewed as much more of an enigma than it has been since the Greenspan days. This, in Warsh’s view, is a positive development, as markets have been far too dependent on being spoon-fed by the Fed for far too long. A bit of volatility should make for greater price discovery and a much healthier market overall.

Fed Funds Rate and Futures Market Expectations

(Expected rate, %)

Greater Equity Market Dispersion Warrants More Active Portfolio Management

With the S&P 500 up 14.9% in the quarter (15.2% total return, which includes reinvested dividends), this was the strongest quarterly increase since the second quarter of 2020, and prior to that since the third quarter of 2009. In fact, since 1927, there have only been 20 quarters out of 395 in which the quarterly increase has been stronger than this past quarter.

What is driving this growth is a combination of strong actual trailing earnings growth and strong expectations for future earnings growth, with analysts raising their expectations that the productivity-enhancing benefits of AI will continue to produce strong growth going forward.

The S&P 500 earnings growth estimate for the second quarter has been revised up from 18% at the start of the quarter to 22.5% today, and for the year as a whole, it has been revised up from 19% to a whopping 26.1%. Most of this is the result of improving earnings growth estimates for the energy, technology, and communications services sectors.

The result has been a compression in the P/E multiple from 22.9x at its recent October peak, to 20.1x by the end of this past quarter. Given that a stock’s return is the sum of earnings growth, dividends and buybacks, and the change in the multiple, such compression, coupled with such a strong market, is unusual. It highlights just which components have been doing the heavy lifting. During the dotcom boom, conversely, P/E multiples soared, as investors’ expectations were far ahead of analysts’ earnings estimates.

The tension between strong earnings momentum and investor sentiment was also evident beneath the surface of the market. During the quarter, the S&P 500 High Beta ETF materially outpaced the S&P 500 Low Volatility ETF, as investor cash rotated away from historically more stable businesses and toward stocks offering greater upside participation. The high-beta trade began to resemble a quasi-leveraged expression of market optimism, with investors prioritizing momentum over balance sheet quality, earnings stability, and downside protection. This can work well during powerful risk-on periods but also subjects the investor to greater volatility, sharper drawdowns, and lesser downside protection if the risk-on trade falls out of favor.

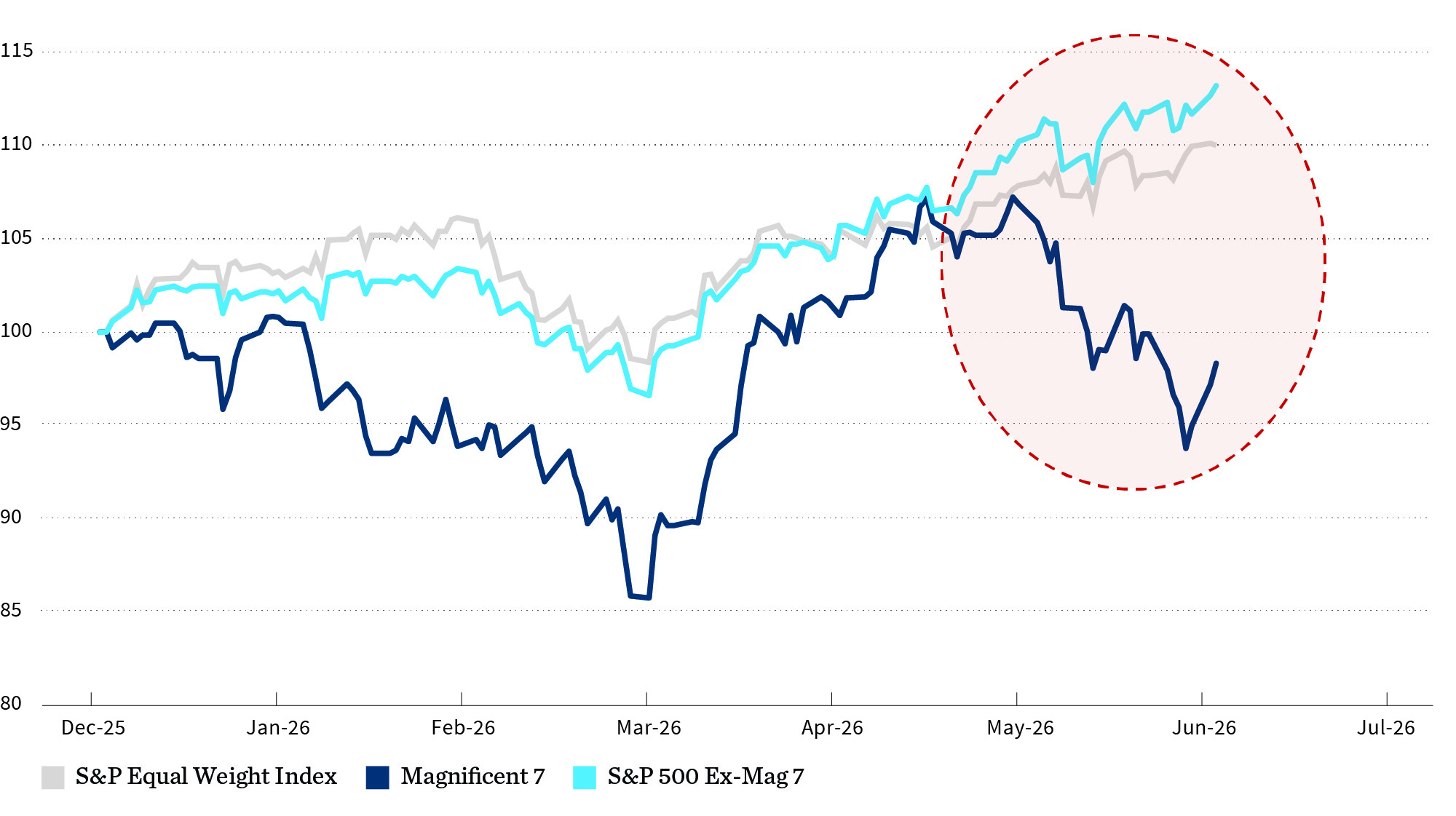

Over the past quarter, some investors have started to raise concerns about the sustainability of this AI investment growth.

The view is that the capex investment taking place is being driven by exceptionally heavy free cash flow use by the hyperscalers, on the basis that it will generate future earnings and cash flows that will more than cover the current high levels of expenditure. However, investors are concerned about what might happen if those future returns do not materialize. For example, if the technology disappoints, cheaper competition emerges from China to erode margins, or the gains are not shared evenly and captured by only one or two winner-takes-all companies, then those earnings growth expectations could start to be revised sharply lower. The result has been that while investors have continued to maintain market positions in AI, they have also begun to look for greater diversification, with rotation taking place within the market (but not out of the market) over the past quarter.

This is depicted in exhibit 3, which shows the Magnificent 7 stocks underperforming while the rest of the market continues to rise. We believe this is a healthy development, in which investors are starting to take advantage of attractive valuations and entry points for many higher-quality stocks (including moving down the cap scale to smaller and midcap stocks) that had been largely ignored during the mega-cap surge.

S&P 500 Index

(Indicies rebased to 100 31 December 2025)

In fact, exhibit 4 further highlights this by showing us that since COVID, we have continued to see a steady decline in the correlation between the S&P 500 and the equally weighted S&P 500. In the second quarter, this correlation fell to its lowest reading on record. What this divergence is telling us is that the largest-cap stocks in the index are behaving very differently from the rest of the index—at first they were soaring while the rest of the market was growing more slowly; now they are falling, while the rest of the market is rising.

1-Year Trailing Correlation of Daily Returns for S&P 500 vs. S&P 500 Equal Weight Index

The above charts highlight the unique period we are in as we study the fine details and dynamics of the investment landscape. We look forward to discussing so many of these topics in our meetings and conversations together as we move into the second half of the year.

Thank you for your trust and confidence,

The 1935 Wealth Management Team

| Index | YTD | 2Q | 1Y | |

|---|---|---|---|---|

| S&P 500 | U.S. Large Cap | 10.21% | 15.20% | 22.32% |

| DJIA | U.S. Large Cap | 9.76 | 13.38 | 20.65 |

| Russell 3000 | U.S. All Cap | 10.88 | 15.44 | 22.82 |

| Russell 2000 | U.S. Small Cap | 22.57 | 21.49 | 40.78 |

| MSCI EAFE | Developed International | 9.44 | 10.82 | 20.23 |

| MSCI EM | Emerging Markets | 23.85 | 24.05 | 43.51 |

| Bloomberg U.S. HY | U.S. High Yield | 1.96 | 2.47 | 5.91 |

| Bloomberg U.S. Agg | U.S. Core Bond | 0.62 | 0.67 | 3.79 |

| Bloomberg Muni | U.S. Muni Bond | 2.32 | 2.50 | 7.03 |

| MSCI U.S. REIT GR | U.S. Real Estate | 17.58 | 12.15 | 21.15 |

Total Returns

Source: FactSet, William Blair Equity Research