AI is reshaping not only the technology and business landscape but also the architecture of global capital markets and capital formation.

The scale and capital intensity of the development of frontier AI—the most advanced models and platforms in the space—have expanded the universe of investors participating in the sector. That has created a multi-layered ecosystem that includes venture capital and growth equity firms, corporate strategic investors, sovereign wealth funds, infrastructure investors, private credit funds, crossover public-market investors, and, increasingly, retail capital through structured vehicles. Companies seeking to access these sources and achieve long-term funding durability must be ready to navigate the differing incentives of these investor groups.

The design and execution of sequenced capital architecture are becoming mission-critical for frontier AI companies, and capital narratives around scale are becoming competitive differentiators in themselves, particularly in the race towards commercial deployment.

It’s also important to understand that the diversity of capital sources funding AI reflects the hybrid nature of AI itself. While AI is often described as a software revolution, the underlying infrastructure required to train and deploy modern AI systems resembles that of capital-intensive industries, such as telecommunications or energy. Training frontier models requires large-scale Graphics Processing Unit (GPU) clusters—which accelerate complex, large-scale workloads—as well as hyperscale data centers and substantial energy supply. Deployment of AI systems increasingly extends into robotics, logistics automation, and industrial applications. Furthermore, unlike prior software cycles, AI requires sustained capital even after product-market fit.

Understanding the Capital Sources

Below is a breakdown of AI’s primary capital sources.

Venture capital remains the early innovation capital behind AI, and AI deals have come to dominate the entire venture capital market, accounting for nearly two-thirds of total deal value.1 In addition, the concentration has been unprecedented, with 41% of all venture capital dollars allocated in the U.S. having gone to just 10 companies.2

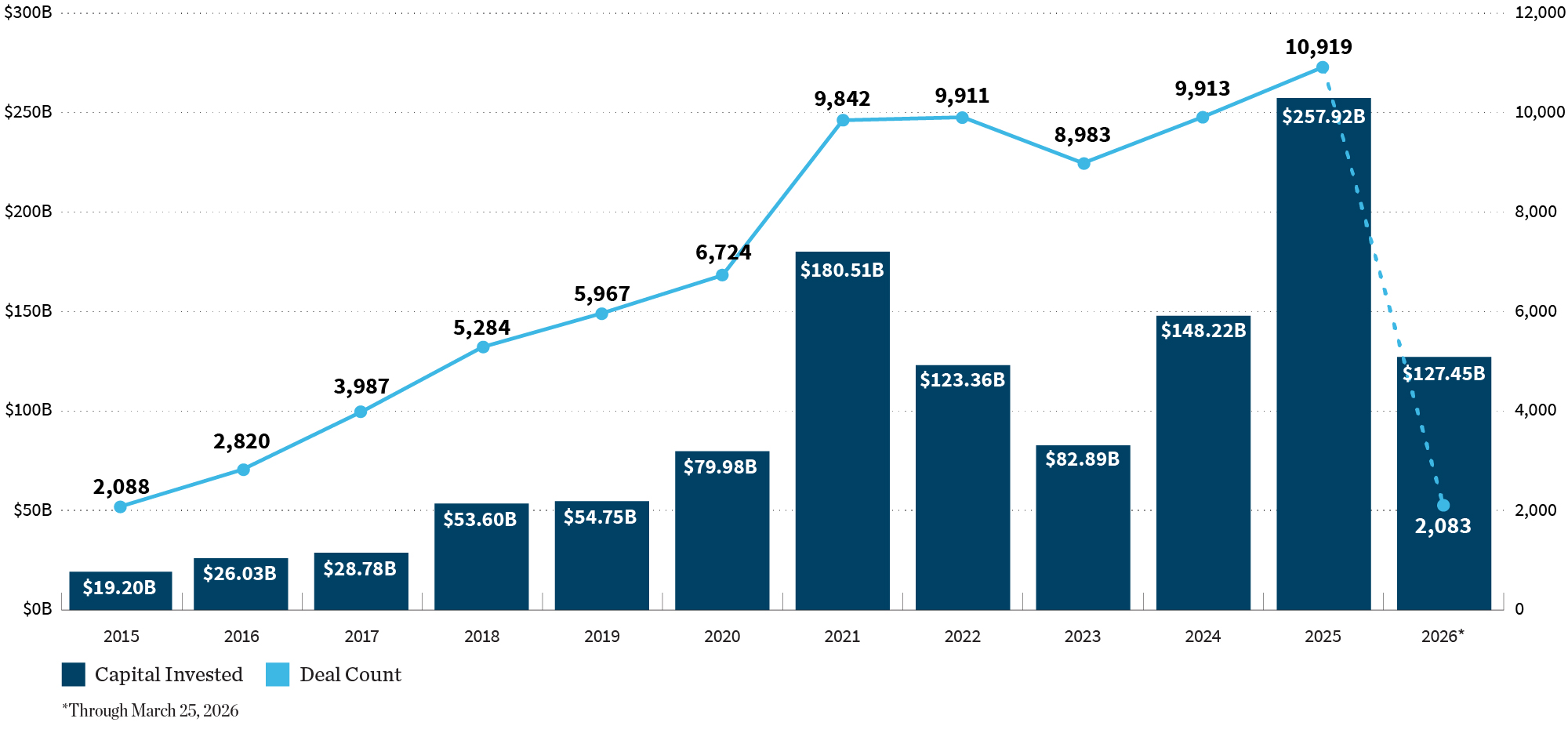

Venture Capital’s Increased Push in AI

Venture capital’s investment in artificial intelligence has increased tenfold over the past decade and is on track for new highs in 2026. VC is just one of the many capital sources fueling the AI revolution.3

Although venture capital remains the financial innovation engine for AI, concerns about the median performance of the asset class as a whole and the lack of returns paid to investors have placed greater focus on liquidity pathways and driven even deeper sector specialization and a less “supermarket” investing approach. However, as financing rounds become harder to access and valuations rise, traditional venture capital is increasingly looking at much earlier-stage AI opportunities.

Corporate strategic investors have become central participants in AI funding, and their capital often comes with agreements on compute infrastructure and commercial deployment, particularly in physical AI.

Strategic investors, especially compared with venture capital, are also focused on how an investment impacts their core business. This approach, built more around long-term ecosystem positioning and strategic capital, can materially reduce burn rate, but it does make platform alignment among partners extremely important.

Sovereign wealth funds bring long-duration capital in part because they increasingly view AI as important for their country’s infrastructure and security. That means they look beyond pure financial returns, underwriting financial ROI, and national or economic objectives simultaneously.

These funds have different objectives, constraints, and liabilities than other capital providers—and lower short-term mark-to-market sensitivity. Additionally, sovereign capital can act as a stabilizing force in late-stage AI financings.

Infrastructure investors and private credit funds are financing the rapid expansion of data centers and energy infrastructure that support AI workloads as infrastructure-style capital models become more common.

Infrastructure investors—funding data centers, power generation, grid interconnections, and other capital-intensive assets—are not betting on a particular AI model; they know AI demand exists and will grow. Private credit funds employ similar thinking but use different means, offering structured debt to compute platforms and infrastructure-heavy businesses, among others.

Crossover investors, including large public asset managers, continue to emerge in AI funding—participating in late-stage private capital rounds. This blurs the line between private and public markets. Still, these investors are anchored in public markets, bringing pricing logic into late-stage private AI, shrinking the gap between private and public valuation, liquidity, and expectations.

Crossover investments occur both pre- and post-IPO, underwriting companies as future public equities. These also facilitate the flow of capital between private rounds, IPOs, and public stock. Compared with venture capital and other categories, crossover investors are less tolerant of valuations that hinge on narrative.

Retail investors are increasingly gaining exposure to high-growth AI companies through special-purpose vehicles (SPVs), separate legal entities created to isolate financial risk, hold specific assets, or execute a dedicated project. Driven by a desire to access leading names and participate in the AI boom, and by a growing sentiment that more value is created before an IPO, SPV participation in private AI shares has surged dramatically in recent years. However, this rapid expansion raises significant concerns, including the often opaque, higher-risk structures of the SPVs, excessive fees, and lack of transparency. The institutional private wealth management channel may play a pivotal role in providing clients with access to these opportunities with fiduciary oversight.

The Importance of Knowledge in a Fast-Moving Market

The above dynamics raise a structural question: if venture capitalists, strategic investors, sovereign funds, crossover investors, and even sophisticated retail investors are already shareholders before an IPO, who will ultimately be the buyer at the IPO?

Additionally, the interconnected nature of AI funding raises some unique issues. For example, private credit funds have been a crucial component in the growth of data centers needed for AI. Still, recent investor redemption pressure in private credit, as well as concerns about AI-driven disruption to their traditional software portfolios, have raised questions. Another example concerns the circular financing used by corporate strategic investors in AI financing rounds.

These issues, which would have been hard to imagine just a few years ago, show how much uncertainty surrounds AI’s incredible rise. But they also underscore why understanding the structure of AI’s capital ecosystem—and the incentives of its participants—is critical for investors and companies navigating this rapidly evolving landscape.

William Blair maintains deep relationships across the capital markets ecosystem, including the sources highlighted above. Our expertise in private capital formation and strategic advisory positions us well to support AI companies navigating the evolving capital landscape and investors participating in the funding of frontier AI.