For many investors, the two most important financial goals are to fund a long and successful retirement and to transfer wealth to family members or charities. With thoughtful planning and strategic management of their portfolios, investors can successfully balance their retirement and wealth-transfer goals.

The current gift-tax exemption creates powerful, tax-efficient opportunities to transfer wealth to your loved ones before you pass away. But you need to ensure you do not give away too much and jeopardize your retirement. Taking a comprehensive look at your current assets and your projected spending needs allows you to effectively balance your retirement and wealth-transfer goals.

To help investors successfully plan for these dual goals, William Blair works closely with clients to help answer three fundamental questions:

- What assets do you currently have?

- How long will your assets last?

- How much can you afford to gift?

What Assets Do You Currently Have?

Identifying Resources to Fund Your Retirement and Wealth-Transfer Goals

The first step in a portfolio review is to identify all the assets you have available to fund your retirement years and wealth-transfer goals. There are many ways to think about your assets, but one helpful strategy is to look at them based on how they will be taxed. Taxes can have a major effect on how much you can accumulate and the net amount available for you to use or give to loved ones. How assets are taxed depends on 1. the type of accounts that the assets are held in, 2. how long you have held the assets, 3. whether the assets have appreciated in value, and 4. the type of asset.

Taxable

Assets held outside of tax-advantaged accounts are typically fully taxable. This means that you will owe tax on any income generated by the assets, including interest, dividends and capital gains upon selling the asset.

- Cash, stocks, bonds, and mutual funds held in non-tax advantaged accounts

- Business interests

- Real estate

Tax-Deferred

Assets held in tax-deferred retirement plans provide an up-front tax break, but the withdrawals or payouts (including all growth on your initial contributions) are fully taxable on the back end.

- Traditional IRA

- Traditional defined-contribution plan

- Defined-benefit plan (pension)

- Nonqualified deferred compensation

- Employer-provided restricted stock

- Employer-provided stock options

Tax-Free

Roth retirement plans do not provide any up-front tax deduction, but qualified withdrawals (including growth) are tax-free.

- Roth IRA

- Roth 401(k), 403(b), 457 plans

How Long Will Your Assets Last?

Understanding Portfolio Longevity

Once you have defined what assets you have, the next step is to think about how long those assets will last. This involves considering the factors that will influence your portfolio’s longevity during the decumulation phase—the period when you are living off your retirement assets rather than earning income and building these resources. Three major factors to consider are inflation, taxes, and market volatility.

Inflation

Inflation can have a major impact over time. Assuming an inflation rate of only 2.25%, something that costs $150,000 today will cost approximately $261,600 in 25 years. Higher inflation rates—which, given history, are likely to occur at some point during your retirement— would, of course, have an even larger impact.

Healthcare

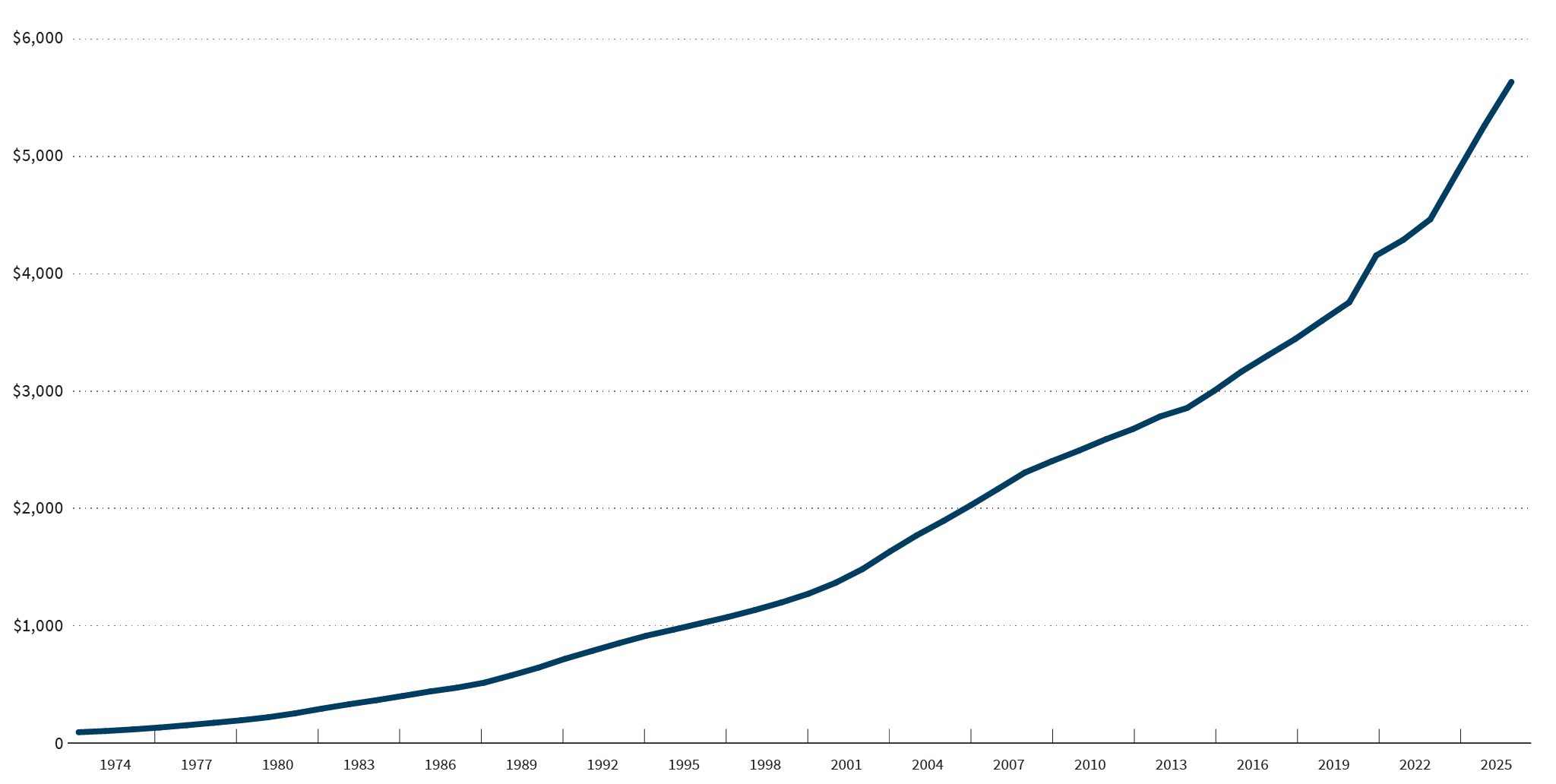

Of all the variables involved in planning for your retirement, perhaps the biggest and most difficult to control is your future healthcare costs. Healthcare costs are increasing much faster than inflation. A 65-year-old couple in the United States will need, on average, $220,000 to cover their healthcare costs over the remainder of their lives. Better healthcare is resulting in longer life spans for many Americans. As life spans increase, we are spending more time in the retirement phase of our lives. That means that your assets will need to last longer than you may have initially thought.

Total Health Expenditures Increases

Total national health expenditures, inflation adjusted, US$ Billions, 1972–2025

Taxes

Federal and state taxes play a large role in determining the longevity of your portfolio. Currently, the top marginal tax rate is 37% and wealthy Americans also face taxes related to Medicare and investment income and limits on the value of the personal exemption and itemized deductions.

Where you live is a major factor in determining the amount of taxes you will pay during retirement. State taxes on income, sales, real estate, and wealth transfer vary significantly from state to state and should be considered when determining whether or not to relocate in retirement.

There are multiple strategies available for reducing your tax liability before you reach retirement. Strategies to consider include maximizing contributions to qualified retirement accounts, funding flexible spending accounts, Roth conversions, and maximizing the use of tax deductions.

Changing State Residency

Moving to a state with lower tax rates can result in significant savings for retirees. But establishing residency in a different state requires more than just spending the majority of your time in the new state. This is especially true for people who maintain residences in multiple states.

To learn more about state tax laws and the rules for establishing residency in a state, download William Blair’s State Residency Changes: Tax Implications and Rules.

Market Volatility

Market volatility always matters to investors, but it matters even more during retirement. During the accumulation stage, as you are saving and investing for retirement, the overall direction of your portfolio performance is much more important than your returns in any given year. There will certainly be periods of positive returns and periods of negative returns, but what really matters is your performance over the long term.

During the retirement, or decumulation phase, however, the magnitude and timing of those negative returns significantly affect the longevity of your portfolio. Because assets are being steadily withdrawn from the portfolio during retirement, market dips that occur early during retirement will have an outsized impact relative to market dips that occur toward the end of retirement.

As a result, it is especially important to take steps to mitigate the risk of market volatility once you reach retirement. Your William Blair wealth advisor can review your portfolio to analyze your exposure to market volatility and help you mitigate this risk within your portfolio.

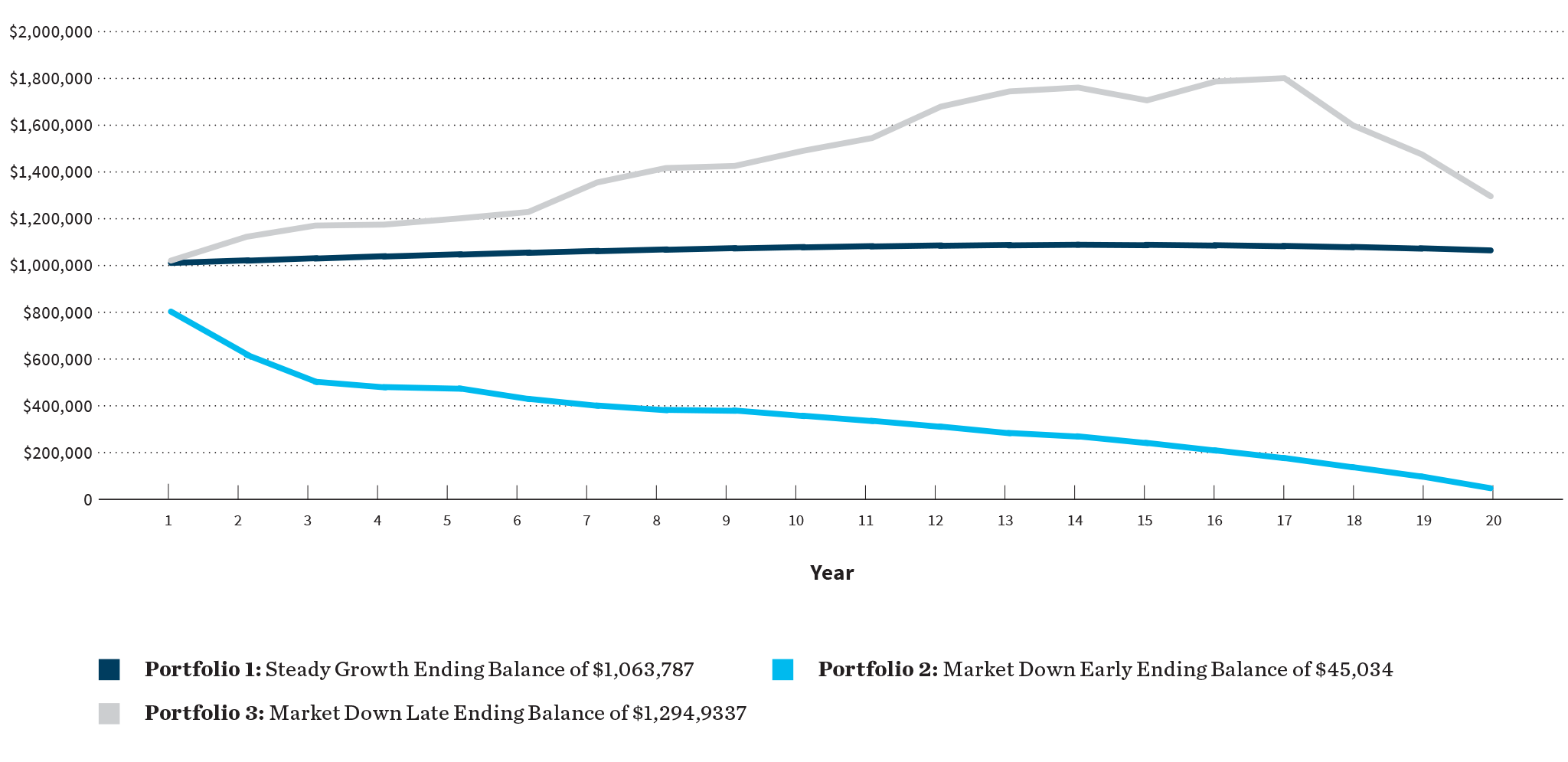

Market Volatility: Timing Matters During Retirement

Each of these three portfolios has an average annual return of 5% over a 20-year period and the same withdrawal rates. But as the chart below shows, the portfolio that experienced losses early on had an ending value significantly lower than the portfolio that experienced losses near the end of the 20-year period.

How Much Can You Afford to Gift?

Identifying Core Assets vs. Surplus Assets

The next step is to determine how much you can afford to give to your heirs. At William Blair, we believe that the best way to approach this decision is to divide your resources into core assets (those that are needed to fund retirement) and surplus assets (those that can be used for wealth-transfer).

Core Assets: Determining Your Retirement Needs

The first priority is to make sure that you do not outlive your assets or have to sacrifice your standard of living during retirement. Drawing on sophisticated modeling techniques, your William Blair wealth advisor will work with you to help you determine how much you are likely to need to safely fund your retirement.

In addition to basics such as housing and medical care, these models also incorporate lifestyle expenses such as travel and entertainment. Other inputs into the analysis are your personal risk tolerance and time frame, as well as conservative—yet realistic—estimates for inflation, market returns, and taxes.

At William Blair, we believe it is not prudent to rely on outperformance to support living needs. The estimated market returns we use are intended to represent beta, or broad market index returns. If the portfolio does outperform the market, however, that will create additional opportunities for wealth transfer.

Surplus Assets: Resources for Wealth Transfer

If your current assets exceed your projected retirement needs, then you may be in a good position to transfer some of these surplus assets to heirs using the current gift-tax exemption.

There are many techniques you can use to take advantage of the gift-tax exemption, from outright gifts to various trust strategies:

- Annual exclusion gifts

- Direct tuition and medical payments

- Grantor Retained Annuity Trust (GRAT)

- Spousal Lifetime Access Trust (SLAT)

- Irrevocable Life Insurance Trust (ILIT)

- Charitable Lead Annuity Trust (CLAT)

- Dynasty Trusts

- State estate tax planning

Addressing Shortfalls

If your retirement resources are insufficient to meet your desired lifestyle needs or wealth-transfer goals, your William Blair wealth advisor can work with you to develop a strategy for addressing the shortfall. Some alternatives include:

- Increasing pre-retirement savings

- Delaying retirement

- Reducing retirement spending plans

- Adjusting portfolio allocation, including enhancing liquidity where possible

- Working part-time during retirement

If you are age 50 or older and are still working, you can take advantage of “catch-up” contributions to further build your tax-deferred or tax-free retirement savings. If you are a business owner or self-employed, you may be able to set up a plan that will allow you to make even larger contributions, such as an individual 401(k) plan or SEP.

Benefits of a Portfolio Review

With the market volatility of recent years, it is especially important to revisit your portfolio to see if it is on track to achieve your retirement and wealth-transfer goals. Recent changes related to the gift-tax exemption amount and tax increases for high-income taxpayers have altered the planning landscape, creating both opportunities and challenges for investors.

At William Blair, we work closely with our clients to help quantify their retirement needs and think strategically about how to transfer any surplus assets to heirs in a tax-efficient manner. We welcome the opportunity to review your portfolio with you and develop a plan for achieving your retirement and wealth transfer goals.

Contact Us: PWM@williamblair.com

Disclosure

This information has been prepared solely for informational purposes and is not intended to provide or should not be relied upon for accounting, legal, tax, or investment advice. We recommend consulting your attorney, tax advisor, investment, or other professional advisor about your particular situation. Investment advice and recommendations can be provided only after careful consideration of an investor’s objectives, guidelines, and restrictions. Any investment or strategy mentioned herein may not be suitable for every investor, including retirement strategies. The factual statements herein have been taken from sources we believe to be reliable, but accuracy, completeness, or interpretation cannot be guaranteed. Past performance is not necessarily an indication of future results. “William Blair” is a registered trademark of William Blair & Company, L.L.C.