When looking at the rapidly emerging distribution tech sector, P&C insurance analyst Adam Klauber notes that, “Shifts in the distribution value chain are the main theme to understand and to watch over time.” Historically, the insurance agent or broker has dominated the value chain, handling areas ranging from customer acquisition to back-end fulfillment. Broker disintermediation is not likely, but the dynamics of the distribution process are shifting and, to a good extent, being automated. The sheer size of the U.S. insurance distribution market, with a total addressable market of over $150 billion, suggests that the opportunity and potential revenue density gains for emerging competitors is large. Demand for changes in insurance distribution is mainly being driven by increased consumerism, a major shift toward digital, and an upgrading of legacy technology. An increasing number and variety of technology-oriented competitors are rising up to fill the gaps in the new distribution chain. Klauber buckets the opportunities into 1) digital aggregators, 2) integrated distributors, and 3) technology enablers.

- Digital aggregators – The digital funnel is rapidly taking share from traditional advertising. Expansion of nascent markets, such as life or homeowners, adds a strong element to long-term potential. The growth outlook is medium to high.

- Integrated distributors – Digital and telesales models are increasing share of the broker commission pie. Well-established in Medicare, this model is morphing quickly into retail P&C markets. The growth outlook is high.

- Technology enablers – SaaS vendors providing solutions to help legacy insurers and brokers compete in the digital space and automate commercial markets. The deep pockets of the buyers mean this sector has a good-sized total addressable market. The growth outlook is medium.

Sizing Up the Market—U.S. Insurance Distribution Spending

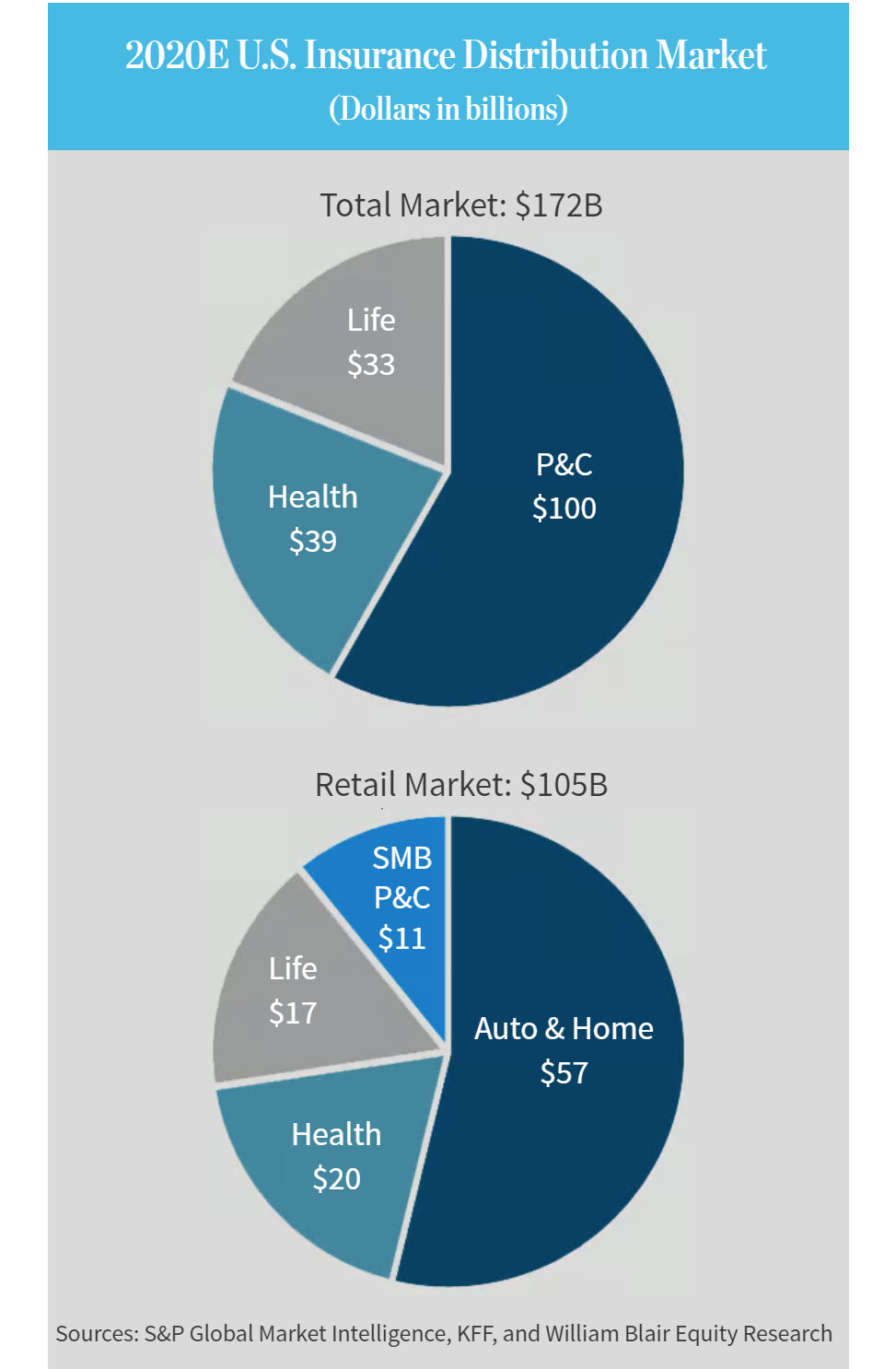

In 2020, Klauber estimates that total U.S. distribution spending by insurance carriers across the property and casualty (P&C), health, and life insurance markets was $172 billion. Within distribution spending, he categorizes expenses as either 1) commissions and other customer-facing expenses (e.g., allocated salaries, agency expense allowances, traveling expenses) or 2) advertising. Over the past three years, total distribution spending has increased at a 7% compound annual rate, with P&C growing 9%, health 7%, and life 2%. Over the past decade, distribution costs have remained relatively consistent as a percentage of premiums, and Klauber expects total distribution spending can grow at a midsingle-digit pace over the long term.

Total U.S. distribution spending was over $170 billion and relatively spread out between the commercial and retail markets, and among different verticals of P&C, life, and health insurance. The retail markets, which represent products sold directly to individuals or small businesses, present strong near- and midterm opportunities, in our opinion. These retail markets include personal auto and home insurance, commercial insurance for small and midsize (SMB) businesses, and health and life insurance sold to individuals (i.e., non-group coverage through an employer or union). In 2020, Klauber estimates the retail distribution spending by insurance carriers was $105 billion. The commercial distribution markets ($70 billion-plus) offer significant opportunities for back-end automaton.

Framing the Opportunity for Distribution Tech—Market Size by Function

Klauber believes that another, potentially more relevant, way to frame the near-term opportunity for distribution tech companies is by function. By function, he means insurance carrier spending on advertising and commissions, and insurance broker spending on technology. Note that the former two categories are included in his distribution market estimate above, while the latter is not. Advertising is the relevant market for digital aggregators, who are at the front end of customer acquisition and connect consumers with insurance brokers and carriers through the internet. Commissions are the relevant market for integrated distributors, which are licensed agencies that handle quoting, binding, and fulfillment of insurance policies often through telesales or online models. Broker IT is the relevant market for technology enablers, which provide software solutions to brokers and carriers to improve broker processes and connectivity between brokers and carriers.

Acquiring insurance customers is an expensive proposition for the insurance industry. The main costs are commission, advertising, and internal functions such as underwriting, running a field agency, and technology and processing costs. While these costs represent roughly 13.5% of total written premiums, they represent over 50% of overhead costs, with agent-based models closer to 60%-plus.

The underlying value chain that drives this high cost system is not broken, but it must evolve. In part, the high cost of the value chain reflects the inherent complexity of creating, underwriting, and distributing insurance products (e.g., a 50-state regulatory system and daunting U.S. legal environment). Nonetheless, Klauber believes high costs are primarily a result of 1) a decades-old customer acquisition process and 2) a patchwork of legacy technology that is suboptimal and not consumer friendly. This suggests that the value chain could simply be modernized and reoriented around the consumer, versus undergoing wholesale disruption.

The decades-old existing distribution chain is not broken, but it is relatively inefficient. The core issue is that the system is bifurcated and highly fragmented. The market consists of 100,000-plus subscale agents selling and processing a multitude of products from hundreds of insurance carriers. In a typical transaction, the insurance company provides the distributor with rough guidelines of desired customers primarily based on rating engines and qualitative preferences. The broker effectively works on a separate track to source the customer and then effectively matches the customer to the insurance company through a wide range of placement practices. Next, the agent facilitates the insurance transaction by providing quotes, filling out the applications, and ultimately connecting with the insurer to bind the policy. The overall transaction process holds true for most types of insurance, whether retail or commercial, or P&C, life, or health.

Klauber stated “We believe a new value chain is coming to the forefront, and an accelerated shift is likely to occur in the next few years. In a fascinating process, the chain is developing across a number of sectors with varied strategies and access points.” He believes there are several common themes:

- The use of technology and analytics to align products and pricing with consumer preferences and needs is occurring rapidly. To a large extent, this trend is being driven by the shift to digital. While retail P&C products are currently leading this trend, it is also beginning to impact commercial P&C, life, and health products.

- Rationalizing and improving the back-end fulfillment process are gaining sizable opportunities in commercial segments. It is not unusual for the process to bind insurance product to take days and even weeks. Real-time and expedited binding capabilities are accelerating at a rapid pace. In a number of products (including commercial), real-time binding is becoming more and more prevalent. Importantly, the ability to leverage technology into back-end policy processes is having marked success in bringing consumerism into the insurance equation.

- Efficient call centers are being used to shift the service burden from the historically subscale CSR.

- Marketing and customer outreach is becoming more efficient. The broker, who has traditionally owned this part of the chain, is not going away but rather is being augmented with alternative means of customer acquisition and service.

For a copy of the “Defining the Distribution Tech Landscape” report mentioned in this article or information on any of the companies in Adam Klauber’s research coverage list, please contact your William Blair salesperson.