Looking ahead to 2023 and reflecting on a dynamic 2022, now is a good time to evaluate your long-term financial plans.

“Taking assessment of your financial plan, reviewing your asset allocation, and thinking about capital deployment for the year ahead are always good practices as we turn into a fresh year,” said Tyler Glover, director of William Blair Consulting Services. “Given the breadth of market changes experienced in 2022, re-evaluating your goals and what makes sense for a long-term strategy becomes particularly important now. Open and ongoing communication with your William Blair advisor should remain a focus in navigating the environment.”

Looking back at the past 12 months, there have been tremendous changes led by the Federal Reserve’s interest rate hikes to tamp down inflation. While 2022 began with rates near zero, they have jumped to 4.25% by December, rising at the fastest pace in decades. Equity and fixed-income markets reacted negatively, both falling during 2022 amid heightened volatility. That’s in contrast to historical relationships, Glover notes, as stocks and bonds typically do not move so drastically or persistently in the same direction—a potential benefit of diversified portfolios.

Asset Diversification

“While rising interest rates have had a substantial influence on bond markets in 2022, we continue to see value long term in maintaining diversification where appropriate,” Glover says. “Even though 2022 has been an unusual year with periods of bonds and stocks moving in tandem, over longer timeframes the two asset classes have generally provided a complementary relationship in balanced portfolios.”

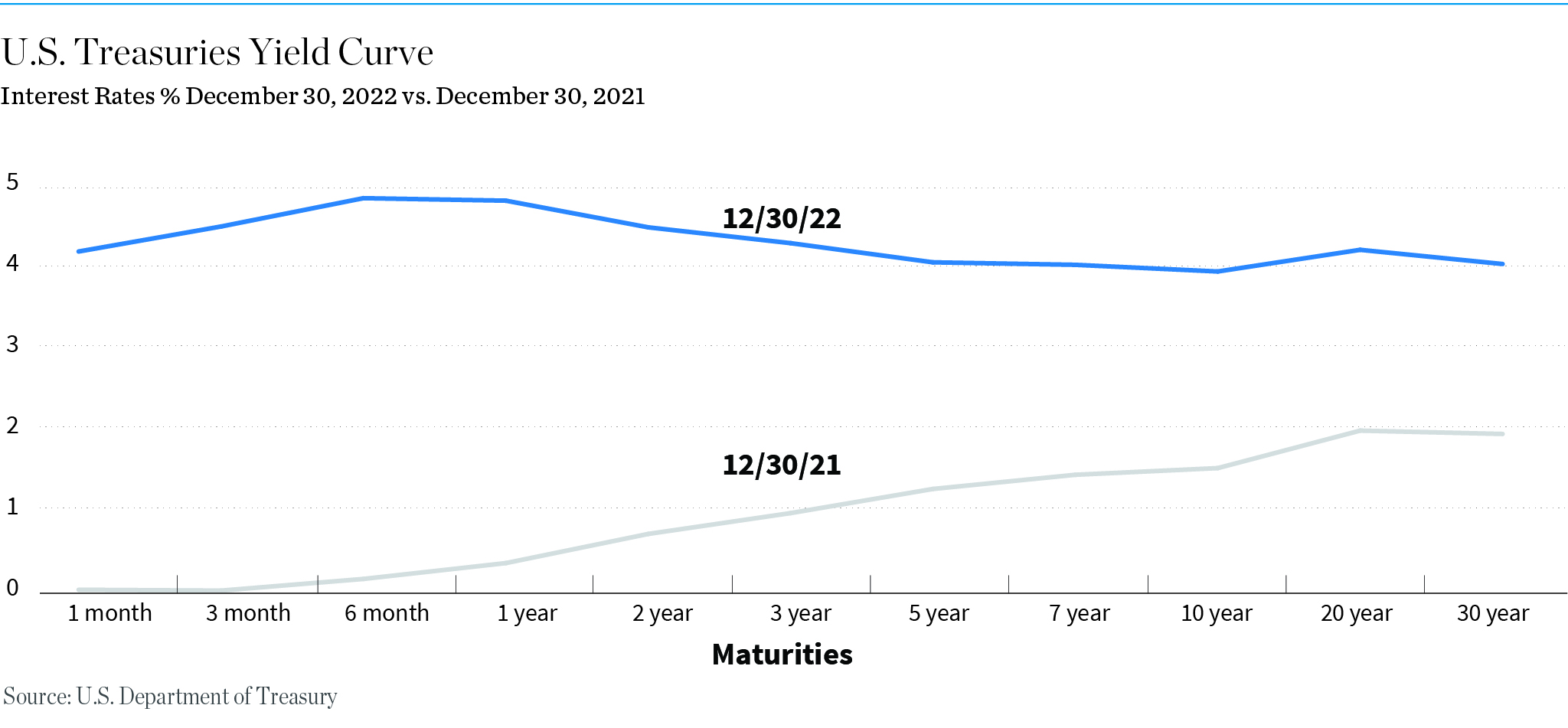

The U.S. Treasury yield curve, which shows the yield of bonds compared with their maturity lengths, also has reacted to the Fed’s action. While the typical yield curve sees long-term bonds having higher rates than short-term bonds, this relationship inverted in 2022 with short-term rates rising on an absolute and relative basis. It’s also an economic indicator of a possible recession—it does not necessarily mean one will occur, but it is a sign that the probability of a recession is increasing.

A silver lining of the interest rate change is it allows for a more reasonable level of yield on fixed-income securities, particularly on the front end of the curve, says Glover. Take the Treasury market for example. Right now, yields on Treasurys with maturities up to one year are providing more than a 4.5% yield, a reasonable yield for a conservative short-term asset relative to recent years.

Diversification also makes sense on the equity front, including investing across market capitalizations.

“We don’t know if we will enter a recession, the duration of that recession, and what it would look like if we definitively go into recession. I think it’s difficult to speculate on those things,” Glover says. “But with history as a guide, smaller-capitalization stocks have often outperformed coming out of a recession.

“For that reason, being aware of relative opportunities, having a degree of flexibility and diversification, and looking at the broader picture can be valuable as well.”

The past year’s change in inflation also impacts financial planning. On the positive side, the IRS has made several adjustments to tax brackets and exemptions reflecting higher inflation. These include nearly a million dollars of additional gift and tax exemptions for 2023 and a big bump up in the amount that individuals can contribute to retirement plans. In regard to estate plans, some strategies are more beneficial in a higher-interest-rate environment.

“Inflation, recession, tighter monetary policies, and geopolitical tensions remain top of mind among investors as we head into 2023,” Glover says. “But continuing to focus on a long-term strategy aligned appropriately with your goals and having an open dialogue with your advisor remains key.”

For more information, contact your William Blair advisor or email Private Wealth Management.

This information has been prepared for informational purposes and is not intended to provide, nor should it be relied on for, accounting, legal, tax, or investment advice. Please consult with your tax and/or legal advisor regarding your individual circumstances. Investment advice and recommendations can be provided only after careful consideration of an investor’s objectives, guidelines, and restrictions. The factual statements herein have been taken from sources we believe to be reliable, but such statements are made without any representation as to accuracy or completeness or otherwise. Opinions expressed are our own unless otherwise stated and are subject to change without notice.