Like other parts of essential services—a broad category that covers everything from pool maintenance to landscaping—roofing has captured investors’ attention. The market is not only massive and fragmented but inherently nondiscretionary, given the enduring need for functional roofs.

Much like the transformation in the HVAC market over the last decade, roofing is emerging as a premier institutional asset class defined by its recession resistant cash flows and a “replacement-over-repair” dynamic that ensures long-term revenue stability. Investors increasingly understand that the roof is not just a structural necessity, but a high-ticket cornerstone of the entire exterior services ecosystem.

This article outlines the roofing sector, discusses why the coming months are primed to be exciting in the space, and provides guidance for navigating the roofing landscape.

What Trends Are Affecting the Roofing Market

The roofing market is divided into two primary categories of demand drivers. The first is lifecycle-driven demand, which makes up most of the addressable market. Demand here is highly predictable and typically occurs when a roof reaches the end of its useful life or some other consumer-driven event occurs (e.g., a move or a cosmetic preference change). In this category, often referred to as “retail,” consumers usually cover the costs, either out of pocket or through financing. Businesses geared toward this part of the market typically, though not always, focus on capturing inbound leads and converting them through diversified customer acquisition channels, including digital, traditional advertising, and organic traffic. Some models have experienced success with direct outreach as well.

The second category is predominantly characterized by weather-driven demand. Here, roof replacements are often necessitated by common occurrences like hail or high winds but can stem from more extreme weather events. Insurers typically bear the cost, and businesses that benefit from this demand channel are usually referred to as having an “insurance model.” Most operators generate leads through direct outreach in affected areas as well as by leveraging referrals and other demand-capture channels. In some instances, leads can come directly from insurance providers.

Companies that intentionally build diversified geographic footprints and have professionalized models designed to methodically convert demand across both lifecycle and weather-driven events are more likely to grow sustainably, positioning them for exit success and investor interest, as we’ll discuss in this article.

Why the Next 12-24 Months Will Be a Critical Inflection Point in Roofing

Roofing is poised to enter a period of strong transaction velocity over the next two years, driven by a combination of maturing private equity platforms and a massive structural replacement cycle. Between 2022 and 2024, the industry saw a groundswell of private equity-backed platform formation. For those vintages, the window for exits at strong valuations is opening precisely as value-creation strategies—such as tech-enablement and regional densification—will be reaching maturity.

This exit dynamic exists despite overall market growth that was below long-term averages in 2025, primarily due to a lack of weather events and some homeowners putting off roof replacements where possible (particularly amid a high-interest rate environment). But America’s housing stock is aged, and homes built in the 2000s housing boom are likely due or overdue for new roofs. The primary driver for roofing demand moving forward is not cyclical, but structural. The U.S. housing market reached its zenith in the mid-2000s, and because standard asphalt shingles have a primary replacement lifecycle of 20 to 25 years, the industry is now entering the “bow wave” of mandatory replacements for the largest housing boom in modern history.

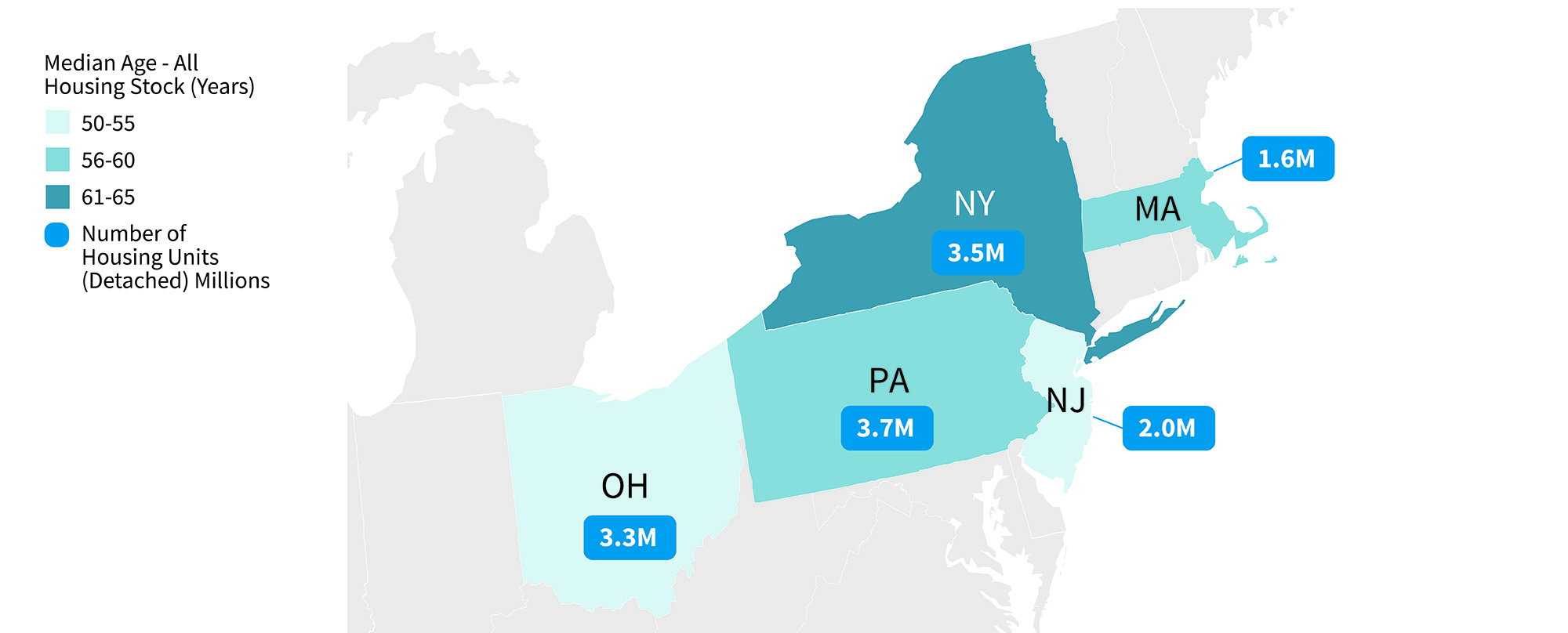

Another factor is the continued consumer shift toward professionalized service levels and expertise, a key component of the broader macro trends associated with “Do-It-For-Me” services in other sectors. Simultaneously, roofing remains in the early innings of consolidation; despite the recent influx of capital, the window for “first mover” scale remains very active. Specific markets appear especially attractive, particularly ones with aging house stock and increasing weather activity. These markets include New York, Massachusetts, Pennsylvania, New Jersey, and Ohio (see map).

Spotlight on Attractive Roofing Markets

Three top markets for roof replacements—Massachusetts, Pennsylvania, and Ohio—have a combined median home age above 60 years with sustained weather event frequency, creating compounding demand drivers. Investors building platforms in these geographies benefit from both structural age and recurring storm activity, rather than relying on a single demand mode.

Lastly, select roofing platforms have driven organic growth over the past two years, even as the sector performed below expectations. That factor supports the case for strong and sustainable go-forward growth in a normalized market scenario, ensuring transaction activity for businesses with strong profiles.

How Roofing Companies Should Navigate Current Trend Lines

Given these converging factors, roofing companies should consider the following strategies—especially if they’re looking for outside investment:

Embrace Lifecycle- and Weather-Driven Demand: Successful roofing operators recognize that market dynamics are split between lifecycle driven and weather-driven demand. To maximize value and maintain operational stability, companies should seek to control their own destiny with strong retail capabilities while remaining structurally agile enough to capture increased capacity when weather-driven events occur.

Leverage Data to Build Geographic Diversification: Investors are seeking platforms that have sustainable demand profiles, often realized through a multimarket presence. Platforms that embrace data and AI to identify the most attractive areas of expansion will build enduring competitive moats.

Employ Diversified Sales and Marketing Capabilities: It will be important for companies to leverage a mix of digital and traditional lead sources and consider the benefits that direct outreach can provide if managed appropriately. The objective is to efficiently move high-intent prospects through the revenue funnel, ensuring a strong capture rate of premium, high-margin projects regardless of the prevailing market catalyst.

Bolster Organic Growth Capabilities: Companies should aim to demonstrate an ability to successfully greenfield new branches in existing or new markets, providing a strong baseline for organic growth. This, coupled with expansion into logical adjacencies (e.g., gutters, siding), helps smooth demand cycles and drive increased LTV.

Focus on Strong M&A Execution and Quantified Integration: Investors are increasingly skeptical of M&A as a primary growth strategy without quantifiable integration outcomes. The bar has shifted from “pipeline depth” to evidence of margin uplift and cross-sell on completed deals. Companies should be prepared to show, by acquisition cohort: revenue uplift through the first 24 months post-close; gross margin trajectory vs. pre-acquisition baseline; and any cross-sell-attach uplift driven by platform infrastructure (e.g., lead routing to gutters, insulation, or siding). Two or three clean integrations with quantified results carry more weight than a 20-name pipeline.

Capture Operational Benefits of Scale: More volume provides the opportunity for larger rebates and lower-priced building materials. Scale also enables investment in technology and talent in ways that differentiate from subscale competitors.

What Investors Want

For owners considering a sale event in the next 12-24 months, the prevailing premium attributes have crystallized. These include: high reroofing mix (more than 85% of roofing-specific revenue from replacement vs. new construction), repeatable, compounding customer acquisition profile with stable acquisition economics (often retail-led or a well-run insurance/retail hybrid), organic growth in the high single digits before M&A, multimarket presence with regional density, and an EBITDA margin profile north of 15%. The gap between platforms that check these boxes and those that don’t will be material over the coming months.

Fueled by attractive attributes, stable end-market dynamics, and evolving consumer behavior, the essential services sector continues to generate massive investor interest. Nowhere is that more evident than in roofing, which has substantial runway, attractive tailwinds, and growing addressable markets.

To learn more about the roofing sector, please do not hesitate to contact the William Blair team.

Disclosure

“William Blair” is a trade name for William Blair & Company, L.L.C., William Blair Investment Management, LLC and William Blair International, Ltd. William Blair & Company, L.L.C. and William Blair Investment Management, LLC are each a Delaware company and regulated by the Securities and Exchange Commission. William Blair & Company, L.L.C. is also regulated by The Financial Industry Regulatory Authority and other principal exchanges. William Blair International, Ltd is authorized and regulated by the Financial Conduct Authority (“FCA”) in the United Kingdom. William Blair only offers products and services where it is permitted to do so. Some of these products and services are only offered to persons or institutions situated in the United States and are not offered to persons or institutions outside the United States. This material has been approved for distribution in the United Kingdom by William Blair International, Ltd. Regulated by the Financial Conduct Authority (FCA), and is directed only at, and is only made available to, persons falling within COB 3.5 and 3.6 of the FCA Handbook (being “Eligible Counterparties” and Professional Clients). This Document is not to be distributed or passed on at any “Retail Clients.” No persons other than persons to whom this document is directed should rely on it or its contents or use it as the basis to make an investment decision.