The transition from a high-growth career to a phase more focused on capital preservation is often a critical inflection point for high-net-worth investors. Years of accumulating wealth through substantial income streams give way to a more deliberate approach to growing and safeguarding capital. As the risks change, the margin of error narrows, and the consequences of decisions may compound more quickly. As a result, proactive planning plays a central role in maintaining financial security and lifestyle objectives.

This piece outlines a structured framework for navigating this shift, highlighting key considerations and strategies to sustain financial security beyond peak earnings.

Understanding the Shift From Peak Earnings

The peak earnings phase is typically characterized by high cash flow. For many professionals and business owners, this generally occurs in their 40s, 50s, and early 60s, when income reaches its highest levels. Earnings are often generated by business ownership or entrepreneurship, senior leadership roles, or liquidity events. At the same time, taxes are higher, spending is elevated, and portfolios are often structured with growth as the primary objective.

As individuals progress out of this phase, financial dynamics can change considerably. Active income streams decrease or cease, placing greater reliance on investment portfolios and other assets as a primary source of cash flow to support lifestyle needs, cover expenses, support family priorities, and preserve purchasing power. At the same time, investors may face a broader set of risks that can compound over time, including inflation, market volatility, geopolitical uncertainty, and regulatory and tax changes.

Drawing down assets rather than building them, or seeing account balances decline even when planned, can feel counterintuitive after decades of focusing on growth. Thoughtful planning helps reframe this phase. Creating defined goals and having regular dialogue with your wealth advisor aligns financial strategy with your evolving personal objectives.

The Wealth Lifecycle

Financial priorities change across distinct stages. For many high-net-worth individuals, the evolution from peak earnings to preservation represents a pivotal inflection point along this broader wealth journey.

| Stage | Primary Focus of Each Stage | |

|---|---|---|

| Accumulation | • Grow income and reinvest earnings • Build assets across retirement plans, equity compensation, business interests, and taxable investment accounts • Align portfolios with long-term objectives |

Growth |

| Peak and Preservation | • Position portfolio to withstand market cycles • Prepare for reduced earned income • Tax efficiency |

Risk Management |

| Utilization | • Portfolios increasingly support retirement funding, family priorities, and philanthropic interests • Focus on sustainable income generation and capital stability • Spending strategies typically become more dynamic |

Income |

| Transfer and Legacy | • Planning turns toward intentional wealth transfer • Review estate structures, governance framework, and charitable strategies • Emphasis on continuity, clarity, and lasting impact |

Stewardship |

Core Considerations for Capital Preservation

William Blair wealth advisors take a disciplined, multifaceted approach to help clients develop strategies intended to preserve capital effectively.

Sustainable Income Generation

How does your portfolio generate a reliable cash flow in the phase following peak earnings? Rules governing withdrawals can be a helpful starting point, but effective income planning goes beyond a single guideline. Market performance is rarely linear, and withdrawal strategies often require flexibility, drawing from different assets at different times depending on market and tax considerations and income needs.

For many investors, the goal is to build multiple sources of income within a broader strategy. Dividend-paying equities, income-producing real estate, and select insurance solutions have the potential to provide dependable cash flow while helping manage volatility.

Your plan may begin by taking inventory of available income sources and understanding the rules governing each. Coordinating withdrawals across these sources can help support lifestyle needs while preserving the portfolio’s long-term sustainability.

Diversification and Risk Management

As reliance on portfolio assets increases, diversification becomes more essential. Concentrated exposure—whether to a single stock, sector, or asset class—can introduce unnecessary vulnerability at a stage when recovery time matters more.

For many high-net-worth investors, diversification extends beyond a traditional portfolio. Private business interests, real estate holdings, and other illiquid assets may represent a meaningful portion of overall wealth. Evaluating how these exposures interact with liquid investment portfolios is an important step in managing risk.

Within the portfolio itself, strategic asset allocation balances growth-oriented investments with assets designed to provide stability, income, and liquidity.

Public equities may be complemented by fixed income and alternative strategies, like private equity or private credit, where appropriate. These strategies can enhance diversification, but they also introduce liquidity constraints and valuation complexity that require careful sizing and long‑term planning. Regular portfolio reviews and rebalancing help ensure allocations remain aligned with market conditions and personal goals.

Tax Efficiency

Proactive tax planning is an important driver of longterm outcomes. Our experts use strategies such as tax aware rebalancing, Roth conversions, charitable giving techniques, and coordinated withdrawal sequencing to help preserve more after-tax wealth without requiring additional investment risk.

Additionally, tax-loss harvesting, asset location, and the thoughtful use of municipal securities may help reduce ongoing tax drag. Irrevocable trust-based gifting strategies, including grantor retained annuity trusts (GRATs), may further align tax planning with family and philanthropic priorities. Over time, these decisions can help manage tax impact and support long-term planning goals. The impact of these decisions becomes more tangible when considering how taxes affect retirement income over time.

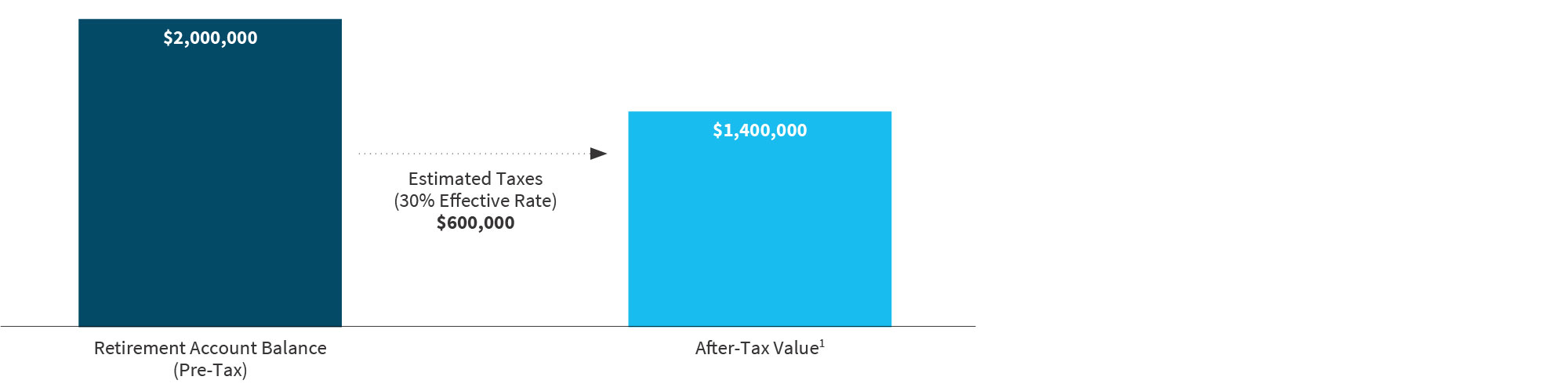

The Impact of Taxes on Retirement Withdrawals

This illustrative example assumes a 30% effective federal tax rate and does not include state taxes.

If a retiree withdraws 4% annually:

- Gross Withdrawal: $80,000

- After-Tax Income (30%): $56,000

That represents a $24,000 annual difference, before considering state taxes, Medicare premium thresholds, or the compounding effects of withdrawals over time. Thoughtful tax planning can help mitigate this impact. In this context, tax efficiency isn’t just about minimizing taxes in a given year—it’s about structuring income to support sustainability over decades.

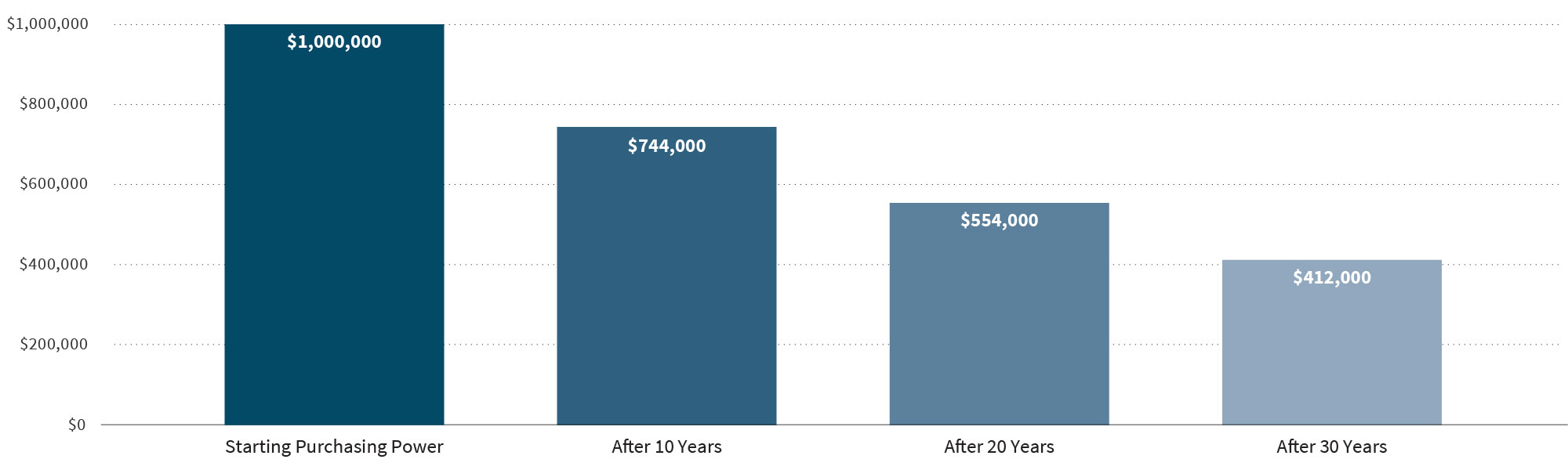

Inflation Protection

Inflation is one of the most persistent threats to long-term purchasing power. Even modest inflation can compound over long horizons, especially when portfolios are funding ongoing spending needs.

The Erosion of Purchasing Power Over Time

This illustrative example assumes a constant 3% annual inflation rate.2

Over a 30-year retirement, inflation at 3% can reduce purchasing power by nearly 60%. When combined with ongoing withdrawals, inflation can accelerate portfolio depletion more quickly than many investors anticipate. Incorporating assets with inflation sensitive characteristics, such as dividend-paying stocks, companies with pricing power, real estate, and inflation-linked securities, like Treasury Inflation-Protected Securities (TIPS), can help preserve real value over time. Regular portfolio reviews with your William Blair wealth advisor can help ensure inflation assumptions and income strategies remain aligned with evolving economic conditions.

Estate and Legacy Planning

As financial independence becomes more secure, many investors shift their attention toward their legacy. Estate planning is no longer just about minimizing taxes; there is a greater emphasis on intention, communication, and stewardship.

Clearly defined structures, thoughtful governance, and early engagement with wealth inheritors can help ensure assets are transferred in a way that reflects family values. Charitable strategies, including donor-advised funds (DAFs) and philanthropic trusts, allow families to integrate philanthropy into their broader financial plans while creating a sense of purpose that extends beyond balance sheets.

Common Pitfalls to Avoid

A common challenge among high earners is maintaining a growth-heavy portfolio. Strategies that worked well during accumulation years may introduce unnecessary risk when portfolios are expected to deliver stability.

Longevity risk is another important planning consideration. Many investors focus on investment returns but underestimate how long they may rely on their portfolios in retirement. The longer assets need to support spending, the greater the potential impact of inflation, healthcare costs, and market volatility over time.

Lastly, emotional decision-making—particularly during periods of market stress—can undermine even well-constructed plans. Establishing an investment policy statement that outlines your investment goals, asset allocation strategies, and risk tolerance can help mitigate this. Discipline, process, and regular communication with your wealth advisor are often the difference between staying on course and unnecessarily reacting at the wrong moment.

Risks to Manage Beyond Peak Earnings

Understanding these risks can help inform more resilient planning strategies as income sources and priorities change.

| Risk | Why It Matters Post-Peak | Planning Consideration |

|---|---|---|

| Longevity | Longer retirements increase portfolio strain | Flexible withdrawal strategies |

| Inflation | Erodes purchasing power over time | Inflation-sensitive assets, like TIPS |

| Sequence of Returns | Early losses can permanently impair income | Portfolio diversification |

| Tax Drag | Lower income means less margin for inefficiency | Asset allocation, tax-aware investing |

Key Questions to Consider

As you transition from wealth accumulation to wealth preservation, a few key questions can help frame the conversation:

- Do I have a clear understanding of my complete balance sheet? Have I taken inventory of my assets and liabilities?

- How dependent is my lifestyle on portfolio income today, and how might that change over time? Which assets are positioned to generate reliable income, and is my portfolio structured to support ongoing spending needs?

- Is my plan positioned to keep up with inflation over the next 20-30 years? Will my current investment strategy help preserve purchasing power over a multidecade retirement?

- Have my tax structures evolved as my income and wealth have changed? Am I making full use of tax-efficient investment vehicles, charitable strategies, and asset location opportunities?

- Does my estate plan reflect my current priorities and family dynamics? Are the right structures in place to support wealth transfer, foster philanthropic goals, and provide clarity for future generations?

These questions can serve as a starting point as you evaluate how your financial plan may need to evolve.

Preserving Capital Beyond Peak Earning Years for Long-Term Financial Security

Case Study: After the Liquidity Event

After three decades of building a successful private company, one client decided to sell their business. The transaction created significant capital and an entirely new financial reality.

For years, the client’s salary came from the business, and most of their net worth was tied to a single asset they understood deeply and controlled directly. After the sale, the client’s focus shifted from “How do I grow this?” to “How do I protect my proceeds and sustain it to support future generations?”

Managing tax exposure from sales, diversifying positions, and building a portfolio capable of generating sustainable income requires careful planning.

Working with their William Blair wealth advisor, the proceeds were repositioned into a diversified mix across equities, fixed income, and select private investments, with an emphasis on tax efficiency, liquidity, and risk management. A flexible withdrawal strategy was designed to adapt to changing market conditions rather than rely on a rigid spending rule.

The result wasn’t just a new portfolio—it was a new framework. The client moved from operating a business to stewarding long-term wealth, with greater clarity around sustainability, legacy, and purpose.

Moving Forward With Intention

Preserving capital beyond peak earnings is not a one-time decision; it’s an ongoing process that can be adjusted as markets, family dynamics, and personal priorities evolve. The most effective strategies begin early, remain flexible, and are guided by a clear understanding of what wealth is meant to support.

For high-net-worth individuals, William Blair experts bring a level of experience and structure to a process that can be complex and decision-intensive. The goal is not just to protect what you’ve built but to ensure it continues to serve its purpose: providing security, flexibility, and opportunity for years to come.

Disclosure

This commentary is for informational and educational purposes only and is not intended to provide, nor should it be relied on for accounting, legal, tax, or investment advice. Please consult with your tax and/or legal advisor regarding your individual circumstances. Investment recommendations and investment advice can be provided only after careful consideration of an investor’s objectives, guidelines and restrictions. Not all strategies mentioned here are eligible or suitable for all investors due to the potential loss of investment, limited liquidity, valuation uncertainty, higher fees and expenses, and complex tax considerations. Past performance is not necessarily an indication of future results. The factual statements herein have been taken from sources believed to be reliable, but such statements are made without any representation as to accuracy or completeness. Opinions expressed are current opinions as of the date appearing in this material only and subject to change without notice.